ETF INVESTING DURING THE PLAGUE

These Corona-Resistant Investment Strategies Might Well Be Profitable For the Rest Of 2020

Both Trend Following and Risk Parity strategies made money this year, when designed properly.

There’s this old one-liner, “How’s the market doing? Oh, some days are up, and some days are down… You know, just like an avalanche”.

Indeed, 2020 has until now offered the worst of all worlds: first a sugar high, then a crash, then a dead-cat bounce where you feel that you are the cat, unless you have a super-natural feel for market timing (which nobody except for your obnoxiously bragging cousin has).

It reminds you of what Lenin supposedly said: “There are decades when nothing happens, and weeks when decades happen”. One would add to Lenin: And there are months when one wants to crawl under a blanket and hope everything goes away. But we are better and stronger than that, so we want to know: what has worked well until now? And do we think this will continue to work?

1) Convertible Bonds, with a shortish moving average

This strategy, in all kinds of variants, has been kicked around the internet for years. I think it was first described by the fantastic Cliff Smith in 2015.

Rule: buy convertible bonds when the sun is shining — that’s when they enjoy a quite good ratio of risk to return. And bail out when dark clouds appear on the horizon.

I use the SPDR Series Trust Barclays Convertible ETF CWB, which is bought or sold according to whether it’s above or below its 4-month moving average. The out of market asset is UST, the 2x leveraged 7–10 year US treasury bond ETF.

Results for the first quarter of 2020: +6.66%.

From 2011 to March 31, 2020: CAGR = +14.93%; maximum monthly drawdown = -7.2%; MAR = 2.07.

Source: Portfoliovisualizer.com.

The results for 2020 are pretty OK (in my humble opinion), because the strategy sold CWB on March 1, at that point buying leveraged treasuries. Since its inception in 2011, no year has been negative.

If you wish to replicate my data, you can do so here.

So, you don’t like this, because it only backtests to 2011? Fair enough — then replace the ETFs with comparable funds such as CNSAX/VFITX, going back to 1998. Result: Spanning decades that included three bear markets, it had only one negative year, namely 2015 (-3.1%.). The dog’s years of 2000 and 2008 earned double-digit returns.

As I see it, the quite short (four months) moving average of this approach enables it to adapt quickly to whatever is happening now. And what worked well in March of this year, is reasonably likely to be OK in the coming months.

2) Drftr’s UPRO/TYD

“Drftr” is the pseudonym of a brilliant, perpetual travelling Dutchman. This strategy is one of his inventions. Like in all other examples here, I have my own skin in this game, and have profited nicely from it during the high and low points of this year.

Again, this approach is simple and easy to implement. The basics: Invest 50% in an S&P 500 ETF during good times, while keeping the other 50% in an intermediate treasury bond fund. When the outlook for equities turns sour (as measured by either a 10 month or 200 days simple moving average) move the 50% equity position to intermediate treasuries as well.

In other words, your money is always to 50% invested in a safe haven, and quite often to 100%. Furthermore, we’re talking intermediate instead of long-term treasuries here, to avoid interest rate risk. We trade monthly.

The trick is that bonds often go up together with stocks, while they also provide a very decent hedge. And the special sauce is to use leverage, so you get enough horsepower out of the times when half of your money is in stocks.

In my case, your stock asset is UPRO, the ProShares UltraPro S&P500 ETF (with triple leverage). And your bond ETF will be TYD, the Direxion Daily 7–10 Yr Trs Bull 3X ETF.

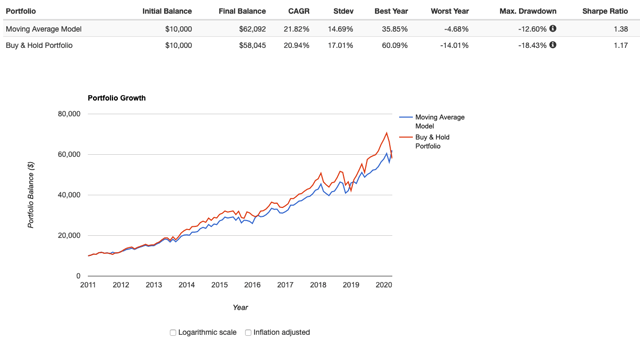

Return, first quarter of 2020: +7.35%.

CAGR from 2011: +21.82%, maximum monthly drawdown: -12.6%. MAR = 1.73.

Source: Portfoliovisualizer.com.

Here is the link to the Portfoliovisualizer backtest.

You don’t like leverage, and you don’t like backtests that are shorter than a decade? Then try the same strategy with SPY and IEF, which are the unleveraged equivalents of our original pair, UPRO and TYD. Then, your test goes back to 2004. In other words, it includes the Up to Right Now Greatest Financial Blow-Up, and your 2020 return is still +2.89%, which is nothing to sneeze at, if you ask me.

For the SPY/IEF combo: CAGR from 2004 +8.25%; maximum monthly drawdown: -6.42%. MAR = 1.29.

Conceivably, if the UPRO sell signal hadn’t been triggered by March 1, then we would have been 50% invested in UPRO during all of March, much to our detriment. Yes, there was some luck involved this year, just like (in the case of SPY/IEF and their equivalents) in 2000, as well as in 2008.

In real life, crashes have not often begun on the first days of the month. Most often, the moving averages give you enough time to respond, if you are listening to them. Such is the character of working with moving averages: they might not work in all cases, but they are a good kind of insurance in most of them.

As a matter of fact, even when using a 430-day moving average, this system would have sold the risky ETF UPRO on March 1! It is only when you go up to and beyond a 440-day moving average that you destroy your 2020 returns. But who’d use a moving average of such length?

3) Risk Parity is alive and well, thank you

This one was invented by Varan. No, I’m not talking about the distant relative of Godzilla; this is merely the pseudonym of a polymath gent with the investing wisdom of decades under his belt.

I like this strategy, because a) it generally performs very well with a quite reasonable drawdown, b) it hasn’t had a negative year since it began in 2011, and c) it hasn’t suffered at all this year.

Rules: Buy four assets out of TQQQ QLD QQQ TMF UBT TLT according to risk parity. (This is a potpourri of Nasdaq ETFs and treasury bond ETFs, with various degrees of leverage). Trade monthly, with the timing period and the volatility period being three months.

(This may sound rather difficult, but using the Portfoliovisualizer backtesting machine, is actually quite simple.)

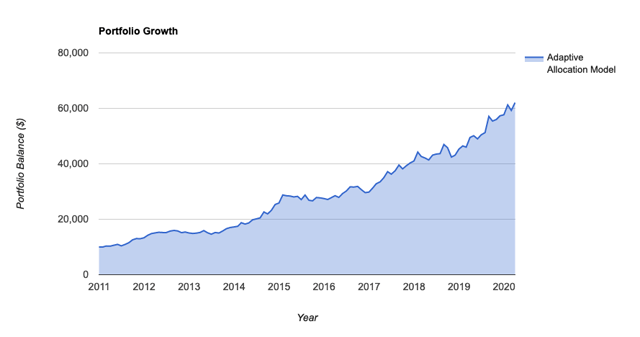

In the first quarter of 2020, this returned +7.59%, which is something I’d write home about.

CAGR from 2011: +21.82%; maximum monthly drawdown: -9.69%.

Source: Portfoliovisualizer.com.

Here’s the link to the strategy.

Anything that has a MAR of over 2 during a crisis of biblical import is something I’d take into serious consideration.

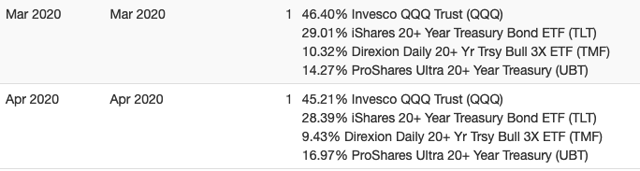

Typically for this kind of risk parity strategy, the monthly rebalancing business is a bit of work. Check out the distributions for March and April:

Source: Created by the author using data from Portfoliovizualizer.com.

If you are sceptical that monthly signals are timely enough, then switch to weekly ones. This comes at a cost to performance: CAGR goes down to 19.33%, and maximum drawdown up to -12.75%. This is still quite good enough for me. I wouldn’t be sure whether the hypothetical future benefits outweigh the costs.

By the way, is this strategy too complicated for you? What are you, lazy? OK, then reduce to the max, and invest only in QLD and TMF. You get more return, but this comes at the price of higher drawdown. MAR has now shrinked a bit, down to around 1.77. It works well on a weekly trading frequency basis, too.

In sum: I was lucky, but you don’t need a lot of luck going forward

The market’s slide started on February 19, so any strategy that rebalances at the beginning of the month — like the ones described in this article — had a good chance to detect the market’s direction, and then react in time.

In contrast, if the markets had for instance waited to crash until the first week of March, these monthly-rebalanced strategies might have suffered quite a bit.

If this is a factor that keeps you awake at night, then switch to a weekly trading frequency. This comes at an affordable cost.

Insurance is never free, you know. Sometimes it is so expensive that one prefers to accept the risk. Black Swan events are typically not incorporated into decision analysis, because doing so is prohibitively costly. But this is not the case here.

(Perhaps I need to install a circuit breaker into these strategies, such as a trailing stop. If you have any ideas how to do so, do let me know.)

All of these strategies do have correlation risk. Switching between stocks and treasuries is generally beneficial, because they generally have an inverse relationship: when one goes down, the other goes up. Will this always be the case?

If you think the U.S. government is going down, and the stock market will become bankrupt, then you need to own gold, or land in Wyoming. In that case, these strategies are not for you.

No matter what: stay safe, and stay healthy. Isolate, and wear that mask. You need good health to enjoy your wealth!

This article was originally published here.